In Nepal, everyone is talking about hydropower development to the tune of 10,000 MW in the next 10 years. This was in fact rightly prioritized in recent budget speech by the finance minister. However, is it so easy to generate electricity from hydro power at this scale (it is estimated investment amounting to US $ 2.75 billion is needed)? Here is my take on the budget speech.

The chairman of Power Trading Corporation of India (PTC), T.N. Thakur, rightly stresses on the need for right institutions to attract shortfall in investment to generate hydro electricity of this scale. Whatever the politicians and ministers say, ultimately the quality of institutions rule! Also, the private sector will not jump into this industry on its own because of huge overhead costs, uncertainty, and risks. The government has to lead the way, give enough confidence to the private sector by sharing risks and costs, build right social and political institutions, and finally let the private sector unleash its magic!!

Q: Does Nepal have the right institutions to create the right kind of environment for the development of hydropower?

Thakur: You have to build some institutions. Today, I am very happy with the government and the politicians I have met, including the prime minister of Nepal. They have at least realized the need for developing hydropower. Prime Minister Pushpa Kamal Dahal is very forthright and businesslike. He has really given a lot of confidence to the people in India, saying that this is the right time to invest in Nepal. I met the Minister for Water Resources Bishnu Poudel and his secretary; I feel that they are eager to meet the target set by the government. I have also called on Deputy Prime Minister Bamdev Gautam and Finance Minister Dr. Baburam Bhattarai. Today, I see tremendous political will to go ahead with the plan to generate 10,000 MW.

Q: Obviously you have met many Nepali officials. What is your assessment?

Thakur: You should have the right kind of institutions here to further your hydropower projects. You have to make a number of institutional reforms and create the right kind of policies. Actually, 15 years ago we were in a similar situation. We invited investment, but private investors were unwilling to put money in India. So the government decided to develop a power market and set up the PTC at the national level. As a result, the PTC buys and supplies energy to power-deficit states as per their demand.

So, the whole thing is that people should feel confident and secure that if you invest in Nepal, the project will go ahead without any hassles and that investors will get their due return. If that sort of confidence is generated, investors will come forward. Otherwise, why would investors come to Nepal and invest when you do not have the right kind of environment and policies. Let us be frank, no investor will come here for charity. They will come here to earn money.

The ADB raises the alarm for South Asian bond market amidst the financial meltdown in the West.

…As global credit markets tighten in the wake of events on Wall Street, the need for Asia, and in particular South Asia, to develop and strengthen domestic bond markets as a source of long term, local capital, has never been more acute.

...Participants shared information on bond market development, and looked at obstacles to further progress. In the case of the five countries of South Asia - Bangladesh, India, Nepal, Pakistan and Sri Lanka - they sought to identify measures that could help them increase the availability of long term, local currency financing. ...While many initiatives have been taken in Asia in recent years to create deep, liquid bond markets, the depth and maturity of such markets varies greatly, with countries in South Asia lagging counterparts in East and Southeast Asia. Typically, governments in South Asia have relied on bank borrowings and external aid as their main sources of finance in the past.

“Financial market diversification supported by well capitalized and judiciously regulated institutions has been at the heart of the tremendous growth that we have witnessed in East Asia,” said Simon Bell, Sector Manager for the World Bank’s South Asia Finance and Private Sector Development group.

There is just a press release; no papers or anything to support or to explain the present status of South Asian bond market. I would love to see more on this front rather than just releasing a press release of ‘he-said-that-she-said that’ format! I would love to explore the development and current status of bond market in South Asia. Hopefully, the ADB will put up files and papers from the conference soon on its website. Or am I missing a whole lot due to ignorance?

Most of the papers available so far are focused on the impact of the financial meltdown on the emerging markets, which overshadows its impact on poor, developing nations.

Here is one paper which analyzes the implications of sub prime crisis in the emerging markets.

This paper discusses some of the key characteristics of the U.S. subprime mortgage boom and bust, contrasts them with characteristics of emerging mortgage markets, and makes recommendations for emerging market policy makers. The crisis has raised questions in the minds of many as to the wisdom of extending mortgage lending to low and moderate income households. It is important to note, however, that prior to the growth of subprime lending in the 1990s, U.S. mortgage markets already reached low and moderate-income households without taking large risks or suffering large losses. In contrast, in most emerging markets, mortgage finance is a luxury good, restricted to upper income households. As policy makers in emerging market seek to move lenders down market, they should adopt policies that include a variety of financing methods and should allow for rental or purchase as a function of the financial capacity of the household. Securitization remains a useful tool when developed in the context of well-aligned incentives and oversight. It is possible to extend mortgage lending down market without repeating the mistakes of the subprime boom and bust.

Here is a nice piece from the NYT about the impact of this crisis in the developing countries that depend on foreign capital and have American-style trade deficits.

…The crisis, by squeezing the flow of capital, threatens countries from the Baltic to Africa that depend on foreign money to finance their deficits.

…There are more than 20 countries with current-account deficits that exceed 5 percent of their economic output, Mr. Strauss-Kahn said, putting them in what the fund considers the endangered category. Mr. Strauss-Kahn declined to name names, but outside economists listed Bulgaria, Estonia, Romania and Turkey as among the red flags in Europe. In Africa, they said, South Africa and Nigeria were worrisome; and in Latin America, Venezuela and Ecuador.

In a paper I had analysed this decoupling/recoupling issue. There are two channels via which shocks are transmitted- trade flow and financial flow. The trade channel usually impacts with a lag but the financial channel is immediate. This is worrisome as it is a possibility that the crisis has got nothing to do with the economic fundamentals of the economy.

Here is one more link from the Center for Global Development. The CGD has a series of thoughtful blog posts from a wide range of experts.

Here is Shanta Devarajan (did I mention that Shanta is now running a new blog, which focuses on Africa; earlier he used to run a blog focusing on South Asia) asserting that despite the US subprime mortgage crisis, South Asia will continue to grow.

Update: Here is an interesting perspective (a socialist twist and anti-capitalist agenda) about the impact of global financial crisis on the workers around the world.

…But this means that taxes from working people are once again being used to rescue capitalists, demonstrating the boundless parasitism of financial elites. Nouriel Roubini, a New York University economist, describes this as “socialism for the rich, the well-connected and Wall Street (i.e. where profits are privatized and losses are socialized).” Meanwhile, the biggest finance capitalists like JP Morgan are gobbling up these distressed capitals at firesale prices — further concentrating capital in the hands of a tiny finance oligarchy.

…An estimated 2.2 million or 1 in every 50 households in the US face foreclosure. Those who continue to own homes would be 20-30 percent poorer in terms of household wealth as home values drop as a result of the collapse in the housing bubble. According to one estimate, a collapse of 30 percent in US home prices from their over-inflated peak would wipe out $6 trillion of household wealth and leave 10 million households with negative equity in their homes — they owe more on their homes than they are worth — increasing the likelihood of a new round of foreclosures and credit losses.

The global credit crunch means reduced capital flows for third world countries who are chronically dependent on foreign capital inflows to pay for older debts, sustain imports from the advanced capitalist countries and paper over chronic deficits they incur as imperialist states plunder their economies.

Most un-industrialized countries who are dependent on exporting agricultural products, raw materials, minerals, low-value added manufactures and services (e.g. business process outsourcing) to the advanced capitalist countries will be faced with shrinking exports due to the combination of depressed consumption in the North.

Aside from being dependent on low-value commodity exports, un-industrialized countries are also dependent on the export of labor, particularly to the wealthy industrialized countries…his means higher unemployment in labor-exporting countries, reduced earnings for foreign remittance-dependent households, and lower consumption spending in the domestic economy.

As financial instruments and stock markets become less attractive to financial investors, speculative capital shifts more into commodities trading such as oil, minerals and agricultural commodities. This is contributing to the precipitous rise in food and energy prices beyond what conditions in the real economy warrant, thereby rapidly eroding the real incomes of the vast majority especially in the third world.

David Pilling argues that it is vital that more labor from low-productivity farm sector migrate to higher-productivity industry so that India achieves an economic growth rate that has power to reduce poverty and increase prosperity in a large scale. He draws out a recent day dichotomy: the tussle between Tata’s Nano factory in West Bengal and protests by farmers displaced from land where the factory is to being built. He argues that if there is to be large scale industrialization, then India better solve these problems and let the process of prosperity roll forward.

…As many as 600m people, or about 47 per cent of China’s population, live in cities, at least 100 of which have swelled to more than 1m inhabitants.

In India…of the 406m labour force in 2000, 78 per cent lived in rural areas against just 22 per cent in towns and cities. The structural transformation from low-productivity farm labour to higher-productivity industry has been painfully slow. Today, agriculture employs about 60 per cent of the workforce but accounts for a measly one-fifth of national output. The predominantly urban, “organised” sector produces 40 per cent of output with just 7 per cent of the workforce.

…India’s information technology and service sector, no matter how dynamic, simply cannot absorb enough labour. To truly shine, India will need millions, perhaps tens of millions, more manufacturing jobs.

…More fundamentally still, as the dispute over land in West Bengal shows, it is hard to engineer mass migration in a democracy. In contrast to 18th century Britain and 21st century China, the vote of a dispossessed Indian peasant is worth the same as that of a would-be industrialist. Collectively, it is worth more. “You have to hand it to Indian democracy,” says Mr Hasan. “It does give you a voice. But that makes it very difficult to negotiate change.”

It is really hard to solve these kind of problems because the poor farmers can easily vote out the party which takes decision in favor of industries trying to displace people from their land to make factories. Term it ironical or whatever, the reality is that this is democracy. The poor farmers have no choice. Same applies for the manufacturing industries because if they cannot get land, then they will not invest.

This is very tricky problem for the politicians. The leftist parties take advantage of these situations and win election on the back of popular slogans. Though low quality or even absence of education and healthcare are one of the roots of these problems, I don’t think they are as important as Pilling thinks in creating this kind of deadlock. A major problem lies in the century old caste system and the scourges associated with it. Remember, India is a very culturally, ethnically, and politically divided country. Let short, quick judgment not overshadow other important constraints!

This book is light read yet a compelling one. You will neither find rigorous arguments, data, and detailed descriptions like you get in books written by Rodrik, Stiglitz, or Bhagwati nor you will find anti-globalization (anti-trade) sentiments resonated in Lou Dobbs’ and, to so degree in, Naomi Klein's books. This is not an intellectually challenging book on globalization but is thought-provoking. It looks more like a journalistic work; reporting style writing and not so surfacial but also not too in-depth analysis! The analysis is heavily skewed towards the plight of working class in the US (and to some degree in the Europe). Steingart dismisses Thomas Friedman's idea that "the world is flat" by arguing that disproportionate gains from trade and globalization do not add up to the world being a flat world.

He accentuates, over and over again, the differences between capital and labor market (labor market is not and cannot be flat) and how cheap labor in China and India are gaining and how middle class is emerging in these countries while in the West there have been erosion of low-tiered jobs and slow erosion of middle class.

He refutes the prevailing notion (on trade related debate) of structural adjustment in the job market by presenting statistics on job losses not only in the low-tier jobs but also in the blue-collar jobs. Meanwhile, service sectors jobs are also not increasing in the West. This means that globalization has been unfair, i.e. it is not producing win-win situation, as predicted by some trade theories, in the West. It is a win-lose situation in the West and a win-win situation in the emerging developing nations like India, China, Vietnam, and Brazil.

He also has objection with the profit-minded capitalists who overlook basic labor and environment standards in factories in China and back-office service companies in India. Steingart is worried that the US will be left behind even in knowledge market as Chinese and Indian government pour in more and more money for research and development; he fears that the next Einstein would be from India or China.

He argues that globalization is not debated as is see in reality. He also presents seven fallacies of globalization debate. His book also contains an interview with Paul Samuelson, who also resonates Steingart's argument (or it might be the other way round) that globalization has produced a win-lose situation in the US and the Europe.

…The war for wealth, a bitter struggle for a share of affluence, and the related struggle over political and cultural dominance in the world, are the real conflicts of our day. The war on terror is overblown, the man in the White House has set the wrong priorities, and the public— deliberately or not—is being kept in the dark over the true extent of the global shift of power and wealth. (pp.ix)

…The opponents and proponents of today’s globalization are united in being mistaken. Without knowing it or wanting it, they are part of a single party one could call “America, Don’t Move.” This party appears on no ballot, never holds party conventions, and has never organized a fund-raiser. It doesn’t send any of its luminaries to appear on Meet the Press or post promotional videos on YouTube, nor does it hire pollsters to investigate the opinions of farmers, housewives, and minorities. (pp.9)

Steingart’s seven fallacies of globalization debate (pp.10-21):

The natural progression for a developed economy is to move from an industry-based to a service-based economy.

Economics and morals have nothing in common.

The new world is flat.

The tide of globalization automatically lifts all boats.

Globalization is a great work of peace.

The nation can no longer do anything for the people in its care.

Globalization is a hot issue.

The flat world is broken!

…Within a period of time that would amount to barely a blip in history, 3 billion additional people and there- fore 1.5 billion new workers joined the world’s labor force and helped bring about an unprecedented shift in the balance of power. The West’s 350 million well-trained but costly workers, who until then had been responsible for a large segment of world production, became a minority almost overnight. (pp.133)

…The world is by no means running out of work, as some claim. As long as the number of goods that are produced, sold, and consumed increases, there can be no loss of jobs. At the beginning of the twenty-first century, the global economy is experiencing one of its biggest growth spurts in decades. Despite the advent of the Internet and industrial automation, the sheer volume of jobs continues to increase. What has changed, however, is the distribution of labor in the context of a global labor market. This labor market is unlimited—but not for the Western worker. (pp.141)

Samuelson’s take on the outcome of globalization:

…The globalization leads to a win-win situation for people in China. That’s true for the poor people in China and for the wealthier people in China. In the United States, the development appears to be very different. Highly specialized and professional members of the workforce will profit, while the run-of-the-mill working-class people will be the losers. It’s a win and lose situation. (pp.267)

…In the globalized society, we will see a deeper split within the developed nations. I think the lower half of the income distribution will be the losers. Globalization means two things: in all probability it means an increase in inequality, and in all probability it also means a loss of serenity. Globalization brings us more prosperity, but it also leads to more uncertainty, tension, and enhanced inequality. In America, it has already led to a cowed workforce. Even for an MIT graduate, things have changed. (pp. 270)

Finally, Samuelson’s advice:

My first piece of advice would be: choose the middle way. There is no substitute for the market mechanism— but the market mechanism has no brain, it has no heart. Without political programs it will inevitably breed inequality. My second piece of advice would be: globalization in its current shape and speed makes the world a more insecure and nervous place. We should try to slow down, and, in our own long-run interest, try to be less aggressive. (pp.274)

Oh, I don’t want to miss this! Samuelson on Keynes and Schumpeter:

…First, I was against Keynes because he was contradicting what all my wonderful professors believed. But finally I decided, am I going to let reality take over or am I going to let ideological reverence prevail? My teacher at Harvard University was Joseph Schumpeter, the famous Austrian economist who had come to Harvard from Weimar Bonn University. Schumpeter was erroneous on the Great Depression. He saw it as a healthy thing. His diagnosis was that the Great Depression was a good thing because it was going to improve productivity. Well, of course it didn’t. Of the 40 most gifted graduates in the physical sciences and the 40 most gifted graduates in the biological sciences, in my first year none had a job for the next year. What good was that going to do for the productivity of the subsequent U.S. economy?

...It used to be said that Schumpeter’s nose was out of joint, that he was kind of jealous of Keynes. He said to me: “You are in favor of Keynes because you are a socialist.” I said: “Professor Schumpeter , I come from the University of Chicago—the citadel of capitalism! When was I ever a socialist? You don’t have to be a socialist to be in favor of Keynes.” And he said: “Well, you are a socialist in the sense that you don’t revere the capitalist system.” Well, that was true. I spent my first 15 years under the rule of pure capitalism, and it had lots of advantages and lots of disadvantages. (pp.165-6)

An analysis of the so-called export-led growth (interesting paper from the IMF… the main point is that solely focusing on export-led through tradable sector might not be wholly right; non-tradable sector led-growth could be as powerful as tradable export-led growth)

My latest Op-Ed published today is titled “Enter Socialism with Inflation”. It is about the quantity and quality of budget presented on September 19, 2008 by Finance Minister Dr. Baburam Bhattarai, to the first elected parliament of the Federal Democratic Republic of Nepal.

Although I am happy that sectoral priorities have been quite upfront and to the point this time- putting hydropower and tourism on the top of priority list- I am not satisfied with the inflated budget, econ-political slogans, policies to tame the private sector, promotion of cooperatives, plans to revive sick and moribund firms, and complete disregard to rising inflation rate. This budget is crafted with a socialist and planner mentality, which might not necessarily lead to a servile state but is certain to screw up individual and private sector incentives, which is the last thing Nepal needs if it wants to see the light of a double-digit growth rate.

Read the full article here. My preliminary notes on this budget article is here. Extended summary of the budget is here.

Sept. 19, 2008 will definitely go down as one of the most important dates in the history of the Federal Democratic Republic of Nepal. On that day, Finance Minister Dr. Baburam Bhattarai presented the first budget, albeit two months late, for the coming fiscal year. The first thing that will be noted in the economic history of Nepal will be the heavy, inflated size of the budget, which amounts to Rs. 236,015,900,000. Another thing that will be noticed with raised eyebrows will be socialist stunts like grand but empty slogans, attempts to restructure and tame the private sector, huge deficit financing and high inflation.

…positive aspects, however, are eclipsed by grand and unrealistic plans, digressive policies to revive sick industries, an ambitious GDP growth rate, ignorance of inflation resulting from increased salaries and deficit financing and unrealistic revenue estimation. Considering the quality of the existing social and political institutions, it will not be long before he realizes that these grand plans and expectations are only good on paper.

…Dr. Bhattarai has waved a socialist wand to tame the private sector, which has been largely unhappy with the budget, by creating a parallel body to foster cooperatives. Make no mistake; this is not an assault on the private sector. However, this is definitely a move that will discourage individual and private sector incentives, which are dearly needed now to stimulate entrepreneurial instinct and increase investment.

By placing the Cooperative Board and the Investment Board -- both to be part of the Economic Council chaired by the prime minister -- on an equal footing, the finance minister has embarked on a grand socialist stunt the like of which has not been seen anywhere in the world for the past two decades. Without a clear demarcation of their responsibilities, the interests of these two boards are sure to collide, particularly in the agricultural sector where there is a real possibility of private sector investment being crowded out. Dr. Bhattarai needs to be reminded that the private sector is more efficient than cooperatives, and that if we want to attain a double-digit growth rate, then the last thing needed is a planner mentality and a clash between cooperatives and the private sector.

…These magnificent plans will also bring down the purchasing power of the rupee. Market prices are going to come under tremendous pressure from deficit financing to the tune of Rs. 42 billion, an increase in wages and allowances, cancellation of debts owed by poor farmers to agricultural banks, injection of money into sick industries and the expected increase in remittances and foreign aid.

The mammoth budget, social security investment, post-conflict reconstruction and investment plans will push inflation over the expected rate of 7 percent for the next one year. Since this jeopardizes the exchange rate in the medium term, diminishes export competitiveness and fosters inflation embedded on expectations, the central bank will be forced to raise the interest rate. This will strain lending and investment thereby putting a question mark on the promise of double-digit growth.

The finance minister has given the country a fresh dose of socialist planning agenda filled with unrealistic promises of double-digit growth and prosperity, and a recipe for rising prices. Yes, this budget will find its place in history as being socialist, inflationary, populist, ambitious and unrealistically grand!

Jeffrey Sachs and Bono are writing a blog for the FT from the MDGs summit starting today. Here is a link to the blog.

Earlier, development economist Paul Collier wrote an Op-Ed in the NYT calling for vigorous pursuit of MDGs, increase in aid, and offering a sense of hope to help the bottom billion.

Easterly would stab this paragraph:

The laggards in the struggle for the MDGs are not the poor countries or their ostensibly corrupt governments. The laggards are the rich world, so full of promises and high rhetoric and so low on delivery. The MDGs are falling short because of a lack of promised financing to put in place the clinics, schools, roads, power, and other investments needed for their success. Six years ago, the rich countries pledged in Monterrey, Mexico to “make concrete efforts toward the international target of 0.7 per cent of GNP in official development assistance.” Yet the United States stands are 0.16 per cent, Japan at 0.17, Italy at 0.19, Canada at 0.28, Germany at 0.37, and France at 0.39.

Paul Colliercalls for a vigorous pursuit of MDGs, increase in aid, and offering a sense of hope to help the bottom billion. In the wake of UN General Assembly starting today, he questions why the UN did not did not act to set international guidelines on taxation and investment in resource rich poor countries, why it did not intervene in Mauritania when a coup was staged recently, why it does not do anything on biofuel scam and the prospects of genetically modified seeds in Africa, etc. As always, Collier’s pieces are thought-provoking, lucid, and to the point.

…Hope makes a difference in people’s ability to tolerate poverty; parents are willing to sacrifice as long as their children have a future. Our top priority should be to provide credible hope where it has been lacking. The African countries in the bottom billion have missed out on the prolonged period of global growth that the rest of the world has experienced. The United Nations’ goal should not be to help the poor in fast-growing and middle-income countries; it should do its utmost to help the bottom billion to catch up. Anti-poverty efforts should be focused on the 60 or so countries — most of them in Africa — that are both poor and persistently slow-growing.

A further weakness with the Millennium Development Goals is that they are devoid of strategy; their only remedy is more aid. I am not hostile to aid. I think we should increase it, though given the looming recession in Europe and North America, I doubt we will. But other policies on governance, agriculture, security and trade could be used to potent effect.

…Why, also, did the United Nations not intervene militarily when the democratic government of Mauritania, another country in the bottom billion, was overthrown by a coup last month? Where is an alternative initiative to open international trade to poor countries now that the Doha round talks have collapsed? Above all, with a five-year-old commodities boom transferring wealth to some of the countries of the bottom billion, where are the international guidelines on taxation and investment that might help these countries convert earnings from exports of depleting minerals into productive assets like roads and schools?

…We need not just a “Year of the Bottom Billion,” but several decades. This session of the United Nations is an appropriate moment to get started.

The IPC has a one pager on Ravallion’s reply to Reddy objections to the methodology used in the calculation of the new global poverty line ($1.25 a day at 2005 PPP prices). This is a much condensed version of a long reply by Ravallion to various objections to the new paper, its methodology, and the new poverty line.

...As Reddy notes, $1.25 is lower than the value in the US of our old poverty line, which works out to be $1.45 in 2005 prices. This has nothing to do with Reddy’s claimed faults in our methods, but stems from the revisions to the PPPs in the light of the better price data from the 2005 ICP; naturally, with higher PPPs in poor countries, the $US value of their national poverty lines falls.

Reddy thinks $1.25 a day is “…far too low to cover the cost of purchasing basic necessities,” He asserts that: “A human being could not live in the US on $1.25 a day in 2005 (or $1.40 in 2008), nor therefore on an equivalent amount elsewhere, contrary to the Bank’s claims.” I have no idea how Reddy reconciles this view with the fact that one quarter of (say) India’s population manages to live below the country’s official poverty line, which is about $1.00 per day in 2005 prices—even lower than our international line.

Here is a piece from the NYT about how the head of the Treasury and the chairman of the Fed- both proponents of liberal, free market idea-, fearing further negative repercussion in the economy emanating from the sub-prime mortgage crisis, changed their the administration’s economic ideology!

…Just like that, Mr. Bernanke, the reserved former Ivy League professor, and Mr. Paulson, the hard-charging former Wall Street deal maker, launched what would be the government’s largest economic rescue operation in modern times, one that rivals the Iraq war in cost and at the same time may redefine Washington’s role in the marketplace for years.

The plan to buy $700 billion in troubled assets with taxpayer money was shaped by two men who did not know each other until two years ago and did not travel in the same circles, but now find themselves brought together by history. If Mr. Bernanke is the intellectual force and Mr. Paulson the action man of this unlikely tandem, they have managed to create a nearly seamless partnership as they rush to stop the financial upheaval and keep the economy afloat.

…Along the way, they have cast aside the administration’s long-held views about regulation and government involvement in private business, even reversing decisions over the space of 24 hours and justifying them as practical solutions to dire threats.

…For Mr. Bernanke, the current crisis is the culmination of a lifetime of figuring how the system works from a theoretical viewpoint…Mr. Bernanke’s research into Japan’s financial crisis in the 1990s reinforced his view that the government had to be aggressive in intervening during market crises.

Interesting discussion about the causes of this crisis here. Intellectuals’ discussion about the crisis here.

In my earlier blog post, I said I was partially happy with the way the budget has prioritized sectors like hydro power and tourism. And, I raised some concerns about the potential rise in price level, which is already close to double-digit number.

Now, that I have read the whole budget speech delivered by the Finance Minister, I have some issues with the earlier confidence about the quality of the budget.

Here is a quick glance at the budget:

Total budget: Rs 236 billion 15.9 million

Recurrent expenditure: Rs 128 billion 516.5 million ( up by 40.6%)

Capital expenditure: Rs 91 billion 311 million (up by 64.5%)

Repayment of loans: Rs 16 billion 189.3 million (down by 1%)

General administration: Rs 111 billion 824.9 million

Development programs: Rs 124 billion 199 million

Financing

Current sources of revenue: Rs 129 billion 215 million

Total foreign assistance: Rs 65 billion 793.8 million (Foreign grant Rs 47 billion 93.2 million, Foreign loan Rs 18 billion 700.6 million) Net budget deficit Rs 41billion 11.6 million

Projections

GDP growth 7%

Agricultural growth 4.5%

Non-agricultural growth 8.3%

Inflation 7.5%

Some good stuff: sectoral priorities, increase in taxes in tobacco and alcohol, subsidy on micro-credit and import of machinery and equipment used for milk processing, emphasis on agriculture, irrigation, poverty alleviation, employment generation, ICT, research, rehabilitation, bail out of poor farmers who own money to banks, etc...

Some bad stuff:

Socialist slogans and very populist budget

Extremely inflated budget...revenue target very unrealistic...

Investment Board and Cooperative Board (to promote private and cooperative sectors) under the Economic Council (which coordinates the two boards' activities and align them with national priority)...this might be easier said than done...what if the interest of these two boards clash? What if the cooperative sector crowd out private investment? Less regard to individual and private sector incentive mechanism...

Deficit financing sure to put upward pressure on price level

Efficiency and productivity are compromised by plans to revive moribund, sick state-owned enterprises like Hetauda Textile Mills, Gorakhkali Rubber Industry, Agricultural Tools Factory of Birgunj, fresh injection of funds to Nepal Airlines Corporation to buy two large aircraft...the problem with these sick policies to revive sick firms is that it just looks at the supply side, completely forgetting demand aspect. It is said that the security forces would buy textiles from these Mills, and agricultural tools would be purchased in the domestic market. However, the demand from the security forces is limited, which means that growth prospect of these sick companies is being compromised. Also, why would people buy agricultural tools manufactured in Nepal at a high prices when they can get the same products at a cheaper price across the border? We might end up making stuff no one uses (recall the wasteful resource investment in the Soviet Union)

Ambitious electric railway projects...at a time when there is more than 30 hours a week load shedding in... from where will the country get electricity to run electric rails?

Lots of loopholes for corruption, especially in social security reforms and debt relief ...no scientific methodology revealed so far

too many commissions without plans for solidifying and consolidating the existing ones

As argued earlier, how can Nepal attain double-digit growth rate in just three years. It is very impractical given the institutional and financing constraints to the economy.

No plans to tackle very rigid social, political, and economic political institutions that have been constraints to economic growth

In general, this budget might please the public but is not friendly to the private sector. In a way, this was expected as the very foundation of the budget is based on socialist ideas of ending feudalism and feudal means of production. Read a related Op-Ed here.

The biggest hurdle, however, would be in implementation of the projects and coordination among numerous new and old commissions. I would be modest and not be too optimistic and too pessimistic! I will try to write an Op-Ed in detail along these lines this week, provided that there won't be too much pressure from the classes I am taking this semester!

Today Finance Minister of Nepal Baburam Bhattarai presented budget of around Rs 236 billion ($3.23 billion) to the parliament. As expected, this year’s budget is bigger than last year’s budget and is already being termed ‘populist’ and ‘inflated’. More here. Read the full budget speech here.

The nice thing about this budget is that it takes sectoral issues seriously this time. It has rightly prioritized hydropower, tourism, and agriculture sector as top industries and has emphasized on the industrialization of agricultural sector. This is exactly what I had argued for in last time’s Op-Ed. I had argued for prioritizing hydropower and tourism sector for now and then to work on creating a good investment climate along with establishment of SEZs so that the sluggish manufacturing industry could be a major player in GDP. The budget has also aimed increase investment in agriculture, which is a good news for a country where more than 70 percent of the population is dependent on agriculture. But bailing out the poor farmers through cash could be very difficult. This mimics the Indian policy of bailing out poor farmers in in last year’s budget.

Long story short, considering the constraints to the economy at present and basing policies on reality, I am partially happy with this budget, which has been more pragmatic and better than I had thought before.

Though agriculture, infrastructure, health and education will be major areas of public investment, the budget will rate hydropower and tourism high on its priority, he added.

Dr Bhattarai indicated that the new government might not continue the past ones' privatization policy. "We will activate public enterprises, then issue their shares to people and employees, and run them under the public-private partnership modality," he said.

He reaffirmed the past governments' actions to deal with loan defaulters stringently. But at the same time, he tagged banks as 'parasites'. "Banks have completely ignored the real sector and focused only on serving able groups. This situation must be corrected," he stated.

However, the aim of achieving a double digit growth within five years (specifically, after two years) is very ambitious and I would need very convincing progress and policies to believe that this will be a reality. Bhattarai wants to take two years to prepare the country to get ready to set off in a double digit growth trajectory. However, given the threats to private property (even the Maoist’s party land reform minister grabbed land by force), bottlenecks in supply side, and sluggish manufacturing sector, I would be very hesitant to aim for a double digit growth rate. In a realistic basis, I would first aim for sustaining present growth rate of 5% for the next two years, then scaling it up by 2% for the next two years, then based on the investment climate and the level of structural changes in the economy, I would aim for a double digit growth rate.

The other issue that is sidelined in this context is monetary policy. Right now, inflation rate (7.7%)is more than the GDP growth rate and is expected to remain higher next year (about 7-8%). The injection of more money in the economy (especially by increasing wages to the tune of Rs 12 billion and bailing out poor debt ridden farmers, increasing expenditure by almost 60%) would put pressure on price level. With shortages of different goods and the advent of big festivals, expenditure is expected to shoot up. Moreover, the full effect of global rise in commodity and fuel prices is yet to be seen in the economy. This central bank would not let inflation rate get out of control (imagine how the IMF would bark at the central bank if this happens!). This means rise in interest rate and dampening of banking credit to firms and individual borrowers. It is unclear how monetary policy would be harmonized with the expansionary fiscal policy.

I don’t think inflation would be a major issue unless it crosses 10% limit. The ‘double digit’ number (inflation, not growth rate) would discourage investors. So, as along as it is under this limit (like in India and China), a slightly inflationary GDP growth rate would be tolerable for two or three years. But, this should not be let built on increasing expectations, which would lead to flight of capital and cash from the country.

Sources of finance:

Out of the estimated sources of financing for the current year, Rs 129 billion 215 million would be borne from the current source of revenue. Out of the total foreign assistance of Rs 65 billion 793.8 million, Rs 47 billion 93.2 million would be borne by foreign grant, and Rs 18 billion 700.6 million by foreign loan. However, there would be a deficit of Rs 41 billion 11.6 million even by mobilising both the sources.

With the same institutions still reigning bureaucracy and the same problems plaguing the economy, I wonder how the current administration is aiming to implement the ambitious budget.

Update: there is an increase in budget for the hydropower and transportation sector (113% and 77.14% respectively). This is a good news on fiscal side (concerns, on monetary policy remains high, as mentioned above.

Rs. 13 billion 910 million proposed for the road transport sector, which is an increase of 77.14 per cent in comparison to the revised expenditure of the last fiscal year.

Rs. 12 billion 690 million proposed for the power sector, which is an increase of 113 per cent in comparison to the revised expenditure of the last fiscal year.

A high-level power sector development committee under the chairmanship of the Prime Minister to be established to materialise the objectives of producing and utilizing 10,000 MW hydro powers in the next 10 years.

I will go over the budget speech in detail after my monetary theory class this afternoon. I will write more about the quantity and quality of stuff on the budget tomorrow.

Jayati Ghosh opines that the current economic slowdown, triggered by the crisis in the Wall Sts starting last year, would affect the poor people in the developing countries. So, what can we do to prop up demand? Well, get back to the Keynesian policies to stimulate aggregate demand, mainly through fiscal policy. Would the impact of current crisis in economies around the globe resurrect the Keynesian ideas, which were like hot potatoes after the Great Depression until when the crisis in the 1970s gave rise to Friedman’s camp?

…fiscal policy and public expenditure must be brought back to centre stage. Across the world, we need significantly increased public expenditure to revive demand in flagging economies, to manage the effects of climate change and bring in widespread use of green technologies, to fulfill the promise of achieving minimally acceptable standards of living for everyone in the developing world.

And, some words on reducing inequality:

Reducing inequalities is not going to be easy. It will require the north to reduce its consumption of scarce resources and carbon emissions, which means some reduction of average consumption generally. It will require the global elite, spread across both developed and developing worlds, to curb extravagant lifestyles. It will require wage shares of national income to rise from their current very low proportions, with corresponding declines in the shares of profits and interest. And it will require governments in the powerful developed countries to recognise that they can no longer call the shots in all important international decision

I don’t exactly understand how curbing “extravagant lifestyles” by global elites would reduce inequality. Is this voluntary or involuntary? I guess income redistribution through progressive taxes and employment opportunities for the poor would be more effective than hoping for the global elite to give up their lifestyles!

I have already discussed about the Doing Business 2009 report in a previous blog post. More on the report here. Here, I will focus on Nepal and South Asia. All the South Asian economies saw their ranking slip by some positions in this year’s report. This does not mean that the countries backtracked on earlier reforms. Other economies reformed more and better than the South Asian economies and hence climbed up the ranking, thus pushing the South Asian economies’ ranking down.

Sadly, on the ten index considered on the report, Nepal did not enact reform on a single one of them. The report flatly states, “No major reforms were recorded” in Nepal. Among the 181 countries considered in the report, Nepal’s overall ranking in the ease of doing business is 121, which is ten positions down from last year’s ranking of 111.

More on Nepal and South Asia:

The report states that it takes 7 procedures, 31 days, and costs 60.20 percent of income per capita to start a business in Nepal.

In the construction business it takes 15 procedures and 424 days (highest in South Asia), and costs 248.40 percent of per capital to get a construction permit.

The rigidity of employment index is 42 (Maldives has the lowest rigidity of employment index), and firing cost is equal to 90 days of salary (Afghanistan has the lowest firing cost in South Asia).

It still takes 3 procedures and 5 days, and costs 6.30 percent of property values to register property (Bhutan has the lowest in South Asia).

According to the report, the strength of legal rights index, which takes into account how collateral and bankruptcy laws facilitate the rights of borrowers and lenders, is 5 in Nepal (Bangladesh and India have the highest value in South Asia). Meanwhile, the strength of investor protection index for Nepal is 5.30 (Bangladesh has the best protection system with an index score of 6.70).

In terms of enforcing contracts, it takes 39 procedures and 735 days, and costs 26.80 percent of claim to enforce contract in Nepal. This shows how rigid and inefficient out courts are to resolve commercial disputes. Bhutan has the lowest costs to enforce contracts. Additionally, for a typical firm, it takes 5 years and 9 percent of estate to go through the process of insolvency.

For a typical entrepreneur, it requires 34 payments and 408 hours per year, and costs 34.10 percent of profit to pay taxes.

Furthermore, it takes 9 documents and 41 days, and US $1764 per container for an entrepreneur to export a typical item from Nepal. In the import front, it takes 10 documents and 35 days, and US $1900 per container to import a typical item.

Sanjay Reddy, in a new one pager from the IPC, argues that the new global poverty estimate ($1.25 a day) just digs dipper into the pitfalls of earlier estimate. He is unsatisfied with the methodology used in the survey. Here is a paper, written by the World Bank economists Ravallion and Chen, Reddy is referring to. Check this one as well (Dollar a day revisited). Here is more from Reddy.

...The new international poverty line is too low to cover the cost of purchasing basic necessities. One could not live in the US on $1.25 a day in 2005, nor therefore on an equivalent amount elsewhere. One’s daily income can be a great deal higher than $1.25 and still leave one unable to fulfill basic nutritional requirements. Since the international poverty line is defined in equivalent purchasing power units, this incoherence is not easy to overcome.

...The PPPs calculated for each country also inappropriately reflect irrelevant information about the pattern of consumption in third countries other than the country in which the price level is being assessed and the base country with which prices are compared (the US). This is because the worldwide pattern of consumption determines the weights placed on different commodities when assessing the price level in each country.

...The underlying source of the problems is the lack of a clear criterion for identifying the poor. We have no basis to conclude that the new set of PPPs generate poverty estimates which are closer to the “truth”.

...The relative extent of poverty in different countries and years, and the estimated trend, is dependent on the base year chosen for the exercise and there is no convincing basis to pick the estimates corresponding to one base year over those corresponding to another.

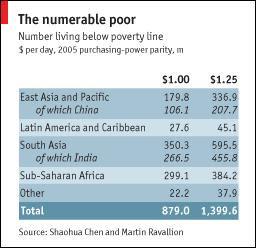

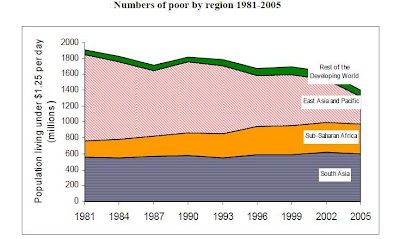

After the WB published new poverty estimate, which upped the number of people living below the global poverty line to 1.4 billion from around 800 million, the Asian Development Bank (ADB) also published its own estimate of poverty line for Asia. The ADB set Asian Poverty Line at $1.35 per day. Here is more about the new global poverty estimate from The Economist.

Stiglitz sees a pattern of deep systemic problems in the events leading to a series of bankruptcy and state bail outs in the economy. In an earlier piece, he puts the blame on "a pattern of dishonesty on the part of financial institutions, and incompetence on the part of policymakers."

We need first to correct incentives for executives, reducing the scope for conflicts of interest and improving shareholder information about dilution in share value as a result of stock options. We should mitigate the incentives for excessive risk-taking and the short-term focus that has so long prevailed, for instance, by requiring bonuses to be paid on the basis of, say, five-year returns, rather than annual returns.

Secondly, we need to create a financial product safety commission, to make sure that products bought and sold by banks, pension funds, etc. are safe for "human consumption." Consenting adults should be given great freedom to do whatever they want, but that does not mean they should gamble with other people's money. Some may worry that this may stifle innovation. But that may be a good thing considering the kind of innovation we had -- attempting to subvert accounting and regulations. What we need is more innovation addressing the needs of ordinary Americans, so they can stay in their homes when economic conditions change.

We need to create a financial systems stability commission to take an overview of the entire financial system, recognizing the interrelations among the various parts, and to prevent the excessive systemic leveraging that we have just experienced.

We need to impose other regulations to improve the safety and soundness of our financial system, such as "speed bumps" to limit borrowing. Historically, rapid expansion of lending has been responsible for a large fraction of crises and this crisis is no exception.

We need better consumer protection laws, including laws that prevent predatory lending.

We need better competition laws. The financial institutions have been able to prey on consumers through credit cards partly because of the absence of competition. But even more importantly, we should not be in situations where a firm is "too big to fail." If it is that big, it should be broken up.

And, Stiglitz throws a punch at those who consistently parrot for minimal regulation:

This is not the first crisis in our financial system, not the first time that those who believe in free and unregulated markets have come running to the government for bail-outs.

Here is a brief analysis from the Institute for Development Studies (IfDS):

...The share price of the commercial banks listed in the stock exchange is very high with no relation whatsoever with the earnings of the concerned institutions. As a result, the capitalized value of the share price of the seventeen commercial banks is Rs. 259 billion, compared with the face value of not exceeding Rs. 30 billion. The main question that must be taken into account seriously by the monetary authorities is the continuity of such bubble in the share price. If such bubble bursts due to any reason, the country will be in a very difficult situation both politically and economically, as the experiences of several developed countries of the recent past suggest.

Nepal's stock market is so insulated to political situation and fiscal and monetary policies that the effect of a change in these variables would be felt in the stock exchange at the beginning of the next such change in the variables! Okay, this might seem a little inflated, but the reality is that the time lag is very long. Also, there are instances when the stock market was indifferent to the changes in fiscal and monetary policies. How could this happen?

Note that there are 21 commercial banks, 58 development banks, 79 finance companies, 12 micro credit banks in Nepal. This for a population of around 26.4 million. Sadly, the handful of commercial banks are awash with liquidity and the poor people are yet to see this being channeled for investment/development purposes.

Hardly anyone is talking about the impact of the Wall Sts meltdown on the developing countries. Here is one view from the WB'S PSD blog. I think the hurricane in the Wall Sts is going to affect the emerging economies more than the developing countries, which have immature financial market and are very loosely, if any, connected to the outside markets. I guess a large part of Sub-Saharan Africa and South Asia would not be affected. East Asian countries, China, India, and other emerging nations might feel some pinch though.

The end of export-led growth: Just last week, Dani Rodrik wrote an article suggesting that the export-led growth that was typical of many Southeast Asian countries will no longer be nearly as viable for the developing world. As he points out, "[t]he most immediate threat is the slowdown in the advanced economies." The collapse of Lehman, the emergency sale of Merrill Lynch, and the troubles of AIG will only exacerbate this slowdown. I suspect Rodrik will look prescient on this one. (China, it seems, is already taking action to deal with an expected drop in demand for exports.)

Financial sector regulation: Stock markets in many emerging markets are becoming increasingly democratized, as the middle class has seen greater access to equities as a vehicle for investment. However, these markets don't yet offer the kind of complex financial instruments seen on Wall Street. Financial authorities in the rest of the world will be watching closely. If U.S. financial markets rebound relatively quickly, the failure of Lehman will be seen as a triumph for creative destruction. The lesson will be that light regulation is best (even though, as Tyler Cowen points out in this NYT's article, Wall Street is not, in fact, as unregulated as is sometimes supposed). If the U.S. sees a prolonged recession, however, I would wager that we will see an impetus for greater regulation of the financial sector in many parts of the world as more complex financial instruments are introduced to emerging markets.

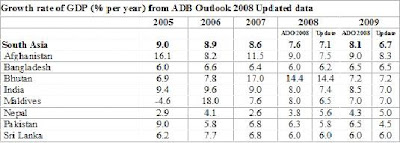

The Asia Development Bank has updated its growth rate projection for the developing countries in Asia. According the updated Asian Development Bank Outlook 2008 Update, regional economic growth for 2008 is scaled down to 7.5% due to "unstable financial markets and rising commodity prices." It projects that the regional growth in 2009 to be 7.2%. Meanwhile, inflation rate is expected to be 7.8% (up from 5.1%) in 2008 and 6% in 2009. Clearly, rising food and fuel prices are pushing up price level and putting strain in GDP growth rates.

The figure below shows statistics for South Asia:

Meanwhile, for Nepal the report shows some encouraging numbers.

GDP growth rate in 2008: 5.6% (up from 2.6% in 2007)

GDP growth rate in 2009 (projected): 5.0%

Inflation as of mid-July 2008: 13.4%

Expected average inflation in 2009: 8.5%

Budget surplus in 2008: 1.9% of GDP (improvement from a deficit of 0.1% in 2007)

Expected budget surplus in 2009: 1.5% of GDP (supported by sustained growth in remittances and tourism receipts)

To the average person, a large rise in unemployment means a recession. By contrast, the economists’ rule that a recession is defined by two consecutive quarters of falling GDP is silly. If an economy grows by 2% in one quarter and then contracts by 0.5% in each of the next two quarters, it is deemed to be in recession. But if GDP contracts by 2% in one quarter, rises by 0.5% in the next, then falls by 2% in the third, it escapes, even though the economy is obviously weaker. In fact, America’s GDP did not decline for two consecutive quarters during the 2001 recession.

However, it is not just the “two-quarter” rule that is flawed; GDP figures themselves can be misleading. The first problem is that they are subject to large revisions. An analysis by Kevin Daly, an economist at Goldman Sachs, finds that since 1999, America’s quarterly GDP growth has on average been revised down by an annualised 0.4 percentage points between the first and final estimates. In contrast, figures in the euro area and Britain have been revised up by an average of 0.5 percentage points. Indeed, there is good reason to believe that America’s recent growth will be revised down. An alternative measure, gross domestic income (GDI), should, in theory, be identical to GDP. Yet real GDI has risen by a mere 0.1% since the third quarter of 2007, well below the 1% gain in GDP. A study by economists at the Federal Reserve found that GDI is often more reliable than GDP in spotting the start of a recession.

Forget about the horrors associated with the "R" word. Read this joke and laugh (or at least, try to laugh):

... when your neighbour loses his job, it is called an economic slowdown. When you lose your job, it is a recession. But when an economist loses his job, it becomes a depression. Economists who ignore the recent rise in unemployment deserve to lose their jobs.

Stiglitz puts the blame on "a pattern of dishonesty on the part of financial institutions, and incompetence on the part of policymakers."

The present financial crisis springs from a catastrophic collapse in confidence. The banks were laying huge bets with each other over loans and assets. Complex transactions were designed to move risk and disguise the sliding value of assets. In this game there are winners and losers. And it's not a zero-sum game, it's a negative-sum game: as people wake up to the smoke and mirrors in the financial system, as people grow averse to risk, losses occur; the market as a whole plummets and everyone loses.

Financial markets hinge on trust, and that trust has eroded. Lehman's collapse marks at the very least a powerful symbol of a new low in confidence, and the reverberations will continue.

Hypocrisy of free market:

We had become accustomed to the hypocrisy. The banks reject any suggestion they should face regulation, rebuff any move towards anti-trust measures - yet when trouble strikes, all of a sudden they demand state intervention: they must be bailed out; they are too big, too important to be allowed to fail.

Eventually, however, we were always going to learn how big the safety net was. And a sign of the limits of the US Federal Reserve and treasury's willingness to rescue comes with the collapse of the investment bank Lehman Brothers, one of the most famous Wall Street names.

I was thinking of blogging on this topic earlier but was unable to find a balanced analysis of the causes behind the tragedy. The political leaders were busy in blame game while villages after villages both in Nepal and India, were being overwhelmed by the Kosi river. Some attribute the flooding, which killed hundreds of people and left millions homeless and forced people to shift to high altitudes, to natural factors. But, Gywali argues that this was a man-made tragedy; it is a product of poor planning and corruption.

The Kosi acts as a massive conveyor belt taking sediment from the Himalaya to the Bay of Bengal. Some one hundred million cubic meters of gravel, sand and mud flow out of the Chatara gorge in mountainous Nepal every year. This flow cannot be blamed on deforestation: we have more forest cover in the Kosi catchment today than ever before. It is caused by Himalayan geotectonics coupled with the monsoon regime. As the river slows down in the flat plains beyond, it deposits its sediment, filling up the river's main channel until it overflows and begins a new course. This natural process produced the large inland delta that lies across southern Nepal and the Indian state of Bihar.

But, for the last half century, the 'Kosi Project' has used embankments to restrict the river's course. This has kept sediment deposits within the main canal, perching the river some four meters above the surrounding land. It was a disaster waiting to happen. Indiscriminate embankment building could never hold back the Kosi's sediment. The river flow at the time of last month's breach was not even high. Rather, it was lower than the minimum average flow for August.

...an Indian scholar writing in Bombay's Economic and Political Weekly, estimated that as much as 60 per cent of the 2.5–3 billion rupees spent annually by the Bihar government on construction and repair works was pocketed by politicians, contractors and engineers. It is said there is a perfect system of percentages in which a share exists for everyone who matters, from the minister to the junior engineer. The actual expenditure never exceeds 30 per cent of the budgeted cost. Contractor's bills are paid without being verified — many of the desiltation and maintenance works allegedly completed are never done at all, and yet payments are made.

This is not directly related to development economics but is interesting in the sense that how incapable our system is to deal with the economic and psychological consequences of failure of a firm seen earlier as a foster child of liberal financial market. Lehman Brothers is now scrambling to find saviors, but in vain . The only road left to explore now is liquidation (which loosely means termination of a business operation by using its assets to discharge its liabilities). In other words, a slow but certain death! What a tragedy for the liberal financial market system!! Chapter 11 protection in high demand, again!

...But that plan fell apart on Sunday, making it likely that Lehman would be forced to liquidate.

What remained unclear was how a liquidation might proceed. One option that was discussed on Saturday would have major banks and brokerage firms continue to do business with Lehman as it unwinds its assets and liquidates over a period of months, according to several people briefed on the discussions. That would buy Lehman time to sell those assets in an orderly way and avoid a fire sale that could depress prices of similar assets held by other banks.

...If no new financing is found before Wall Street opens on Monday, Lehman will have to seek so-called Chapter 11 bankruptcy protection.

Here is WSJ on why didn't Lehman use Fed's discount window?

Why wouldn’t Lehman borrow? For one thing, it may not need to. As in the case of Fannie Mae and Freddie Mac, one of its key problems is with capital and not short-term funding. Another possibility: Taking a discount window loan while everyone is watching for it — and expecting it — might create a new set of confidence problems. Because there was no borrowing leading up to this week, Lehman would’ve been tagged as the borrower of any loan taken out. (The Fed does not disclose the identities of the borrowers.) One way around it would be for several other firms — healthier ones — to step up and offer cover, taking loans and somehow signaling publicly that they also had done so. Another would be to wait until the weekly reporting period ended Wednesday and then borrow on Thursday, allowing a week of breathing room before the next report comes out.

1) Dani Rodrik questions whether export led growth strategy still fulfills its purpose (of stimulating growth).

Many countries are trying to emulate this growth model, but rarely as successfully because the domestic preconditions often remain unfulfilled. Turn to world markets without pro-active policies to ensure competence in some modern manufacturing or service industry, and you are likely to remain an impoverished exporter of natural resources and labor-intensive products such as garments.

Nevertheless, developing countries have been falling over each other to establish export zones and subsidize assembly operations of multinational enterprises. The lesson is clear: export-led growth is the way to go.

(The title of this piece is similar to the title of Paul Krugman's 1987 paper: Is Free Trade Passe?)

2) Jones, Ocampo, and Calice propose channeling 1 percent of developing countries' foreign-exchange reserves to investment in infrastructure.

Although economic growth and poverty reduction in many developing countries has been impressive in recent years, a significant increase in investment in areas such as infrastructure is required to sustain such growth in the future. We propose that a very small portion of developing countries’ total foreign-exchange reserves – say, 1% – be channeled to the expansion of existing regional development banks or the creation of new ones that would invest in infrastructure and other crucial sectors.

Indeed, infrastructure investment is recognized as a key ingredient in sustaining and accelerating growth. However, there is a large financing gap. According to the World Bank, developing countries spend an average of 3-4 % of GDP on infrastructure every year, compared to an estimated 7% of GDP required to meet existing infrastructure needs for maintaining rapid growth. This translates into an annual gap of at least $300 billion at current prices.

3) Pedro de Araujo urges to increase condom distribution and awareness among the poor and uneducated in India to avert rising risk of HIV infections.

HIV knowledge in the Indian population is very poor. Seventeen percent of males and 40% of females say that they have never heard of HIV/AIDS. These numbers are much higher when compared to responses from populations of sub-Saharan African countries. Those who said they knew of AIDS were not necessarily very knowledge: when asked if a healthy looking person could have AIDS, 27% of males and 38% of females did not know the answer. These statistics raise some concerns as to how inadequately prepared the population is in the advent of an outbreak. Another point of concern is the reported levels of stigma in the population. Thirty six percent of males and 37% of females would not buy vegetables from an HIV-infected person. This variable is the most commonly used proxy to measure stigma in these surveys.

...Even though a great part of the Indian population is faithful and abstains from sex, there are still large segments of the population at risk of contracting HIV. Because condom use is very low and knowledge about the disease is very poor, especially with respect to females and poorer and uneducated single males, preventive policies should be targeted at these groups by increasing condom distribution and awareness, increasing substantially HIV/AIDS basic education, and promoting women’s empowerment particularly with respect to sexual choices.

Paul Krugman explains what Keynes really meant when he said "In the long run we are all dead."

Keynes's famous remark "In the long run we are all dead" is more widely quoted than understood. Here is how Krugman explains it: "What he meant was recessions may eventually cure themselves. But that's no more a reason to ignore policies that can end them quickly than the fact of eventual mortality is a reason to give up on living."

This one is from an interview done by Subramanian for IMF's Finance & Development magazine. Read the full interview here. Not a new interview but could be a refresher (...to fend off 'hungoverness' on Saturday morning)...