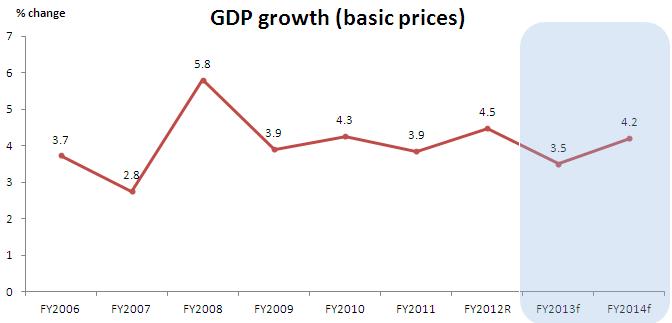

The Asian Development Bank (ADB), in its flagship publication Asian Development Outlook (ADO) 2013 released today, forecasted Nepal’s GDP growth at 3.5% for FY2013 (2012/13) and 4.2% in FY2014. Furthermore, the ADO 2013 estimated regional economic growth in the Asia Pacific region to pick up to 6.6% in 2013 and reach 6.7% in 2014.

This year’s ADO focuses on Asia’s energy challenge. It notes that:

-

Developing Asia's energy needs will expand in tandem with its growing economic influence, but its own endowment is insufficient;

-

Expanding renewable energy sources will not be enough to meet future demand. Consequently, Asia needs to invest in making conventional power cleaner and more efficient; and

-

Asia must aspire to the degree of regional cooperation and integration in energy by 2030 that currently prevails in Europe.

Below are highlights from the Nepal chapter of the ADO 2013:

Economic performance in FY2013

GDP growth

-

Growth to rebound to 4.5% in FY2012

-

Agriculture sector grew by 5.0%, the highest in 4 years

-

Services sector grew by 4.5%

-

Industry sector continued to perform poorly (growth dropped to 3.0% in FY2012 from 4.4% in FY2011) -- Unfavorable business and investment climate (labor disputes, persistent electricity shortages, political uncertainties)

-

-

Inflation eased to 8.3% in FY2012 (food prices declined during most of the year)

-

Stubbornly high inflation caused by:

-

Rising prices of non-food items (reflected by inflation in India)

-

Upward adjustment of administered fuel prices

-

Depreciation of Nepali rupee against third world currencies

-

Rising wages

-

Persistent supply-side constraints (power outages; market distortions by monopolists and monopsonists; infrastructure hiccups; strikes)

-

-

Budget deficit narrowed narrowly to 2.2% of GDP in FY2012

-

Lower capital expenditure

-

Greater revenue mobilization

-

Increase by 22.5%, reaching 13% of GDP

-

Improved efficiency in tax administration and widening of tax base

-

-

-

Not a desirable outcome for a country with large development needs and significant absorption capacity as well as multiplier effect from investment in infrastructure

-

Total expenditure was 20.4% of GDP, slightly higher than in FY2011

-

High recurrent expenditure, reaching 15.6% of GDP in FY2012 from 12.4% of GDP in FY2011

-

To cover large subsidies on fuel and ad hoc expenditure programs

-

-

-

Capital expenditure low, dropped to 3.3% of GDP in FY2012 from 6.5% of GDP in FY2011

-

Lower project disbursements due to lack of timely budget

-

Sharp drop in capital spending allocation itself

-

Monetary sector

-

Central bank’s proactive role and corrective policies led to containment of the fallout of real estate and housing prices

-

Robust remittance inflows boosted deposits and increased liquidity

-

Interbank rates dropped to 1.1% in FY2012 from 8.1% in FY2011

External sector

-

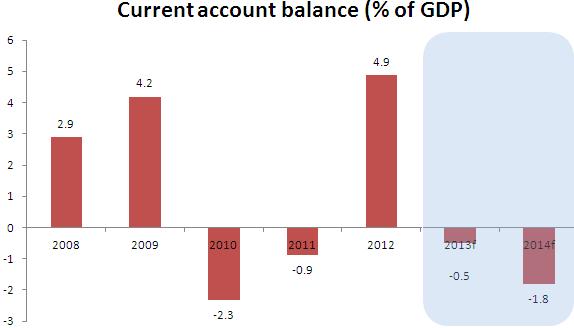

Current account recorded a large surplus of 4.9% of GDP in FY2012 from negative 0.9% in FY2011

-

Massive rise in remittance inflows

-

Modest import growth of 4.5% relative to export growth of 5.4%

-

-

Overall balance of payments surplus reached $1.6 billion

-

Foreign exchange reserves reached $4.2 billion, enough for 7.9 months of import of goods and services.

Prospects for FY2013 and FY2014

GDP growth

GDP growth in FY2013 expected to decline

-

Unfavorable monsoon

-

Shortage of fertilizers

-

Low business confidence

-

Lack of full budget

-

Subdued growth in India

GDP growth in FY2014 expected to rebound

-

Favorable monsoon

-

Adequate fertilizer supply

-

Timely and full budget

-

Moderate expansion of remittances

Inflation

Inflation in FY2013 expected to increase

-

Lower agriculture harvest

-

Wage pressures

-

Upward adjustment of administered fuel prices

-

Power shortages

-

Supply-side constraints

Inflation in FY2014 expected to moderate

-

Good harvest

-

Underlying pressures of FY2013 to persist

-

Cautious policies

External sector

Trade deficit to markedly widen in FY2013

-

Exports growth to decline

-

Subdued growth in India

-

Sluggish activity in Euro area and the US

-

Rising cost of production

-

Imports growth to sharply increase

-

Driven by remittances (lag effect as well)

Current account balance to be negative

-

Wide trade deficit

-

More moderate remittance growth

Fiscal sector

Lack of a full-fledged budget for FY2013

-

Revenue policy guided by Finance Act 2012

-

Capital budget allocation and actual expenditure low

-

Impressive revenue mobilization

-

Domestic borrowing not allowed

-

Fiscal deficit may marginally widen

Moving forward, a full and timely budget for FY 2014 is essential

-

Timely passage to allow for change in revenue policy, allow for domestic borrowing , and accelerate development activities

-

Quality of public spending, aid effectiveness and governance issues need to be addressed